Proof that costs are coming down, reforms working

Florida homeowners insurance rates continued their decline in 2024, ending the year with a net industry average decrease for the first time in two years. The Office of Insurance Regulation (OIR) fourth quarter 2024 QUASR report shows average premiums fell 0.7% between the third and fourth quarter, according to reporting by Ron Hurtibise in the South Florida Sun Sentinel. It’s further proof that the Florida property insurance market is recovering following the legislative reforms from 2022 and 2023.

Florida homeowners insurance rates continued their decline in 2024, ending the year with a net industry average decrease for the first time in two years. The Office of Insurance Regulation (OIR) fourth quarter 2024 QUASR report shows average premiums fell 0.7% between the third and fourth quarter, according to reporting by Ron Hurtibise in the South Florida Sun Sentinel. It’s further proof that the Florida property insurance market is recovering following the legislative reforms from 2022 and 2023.

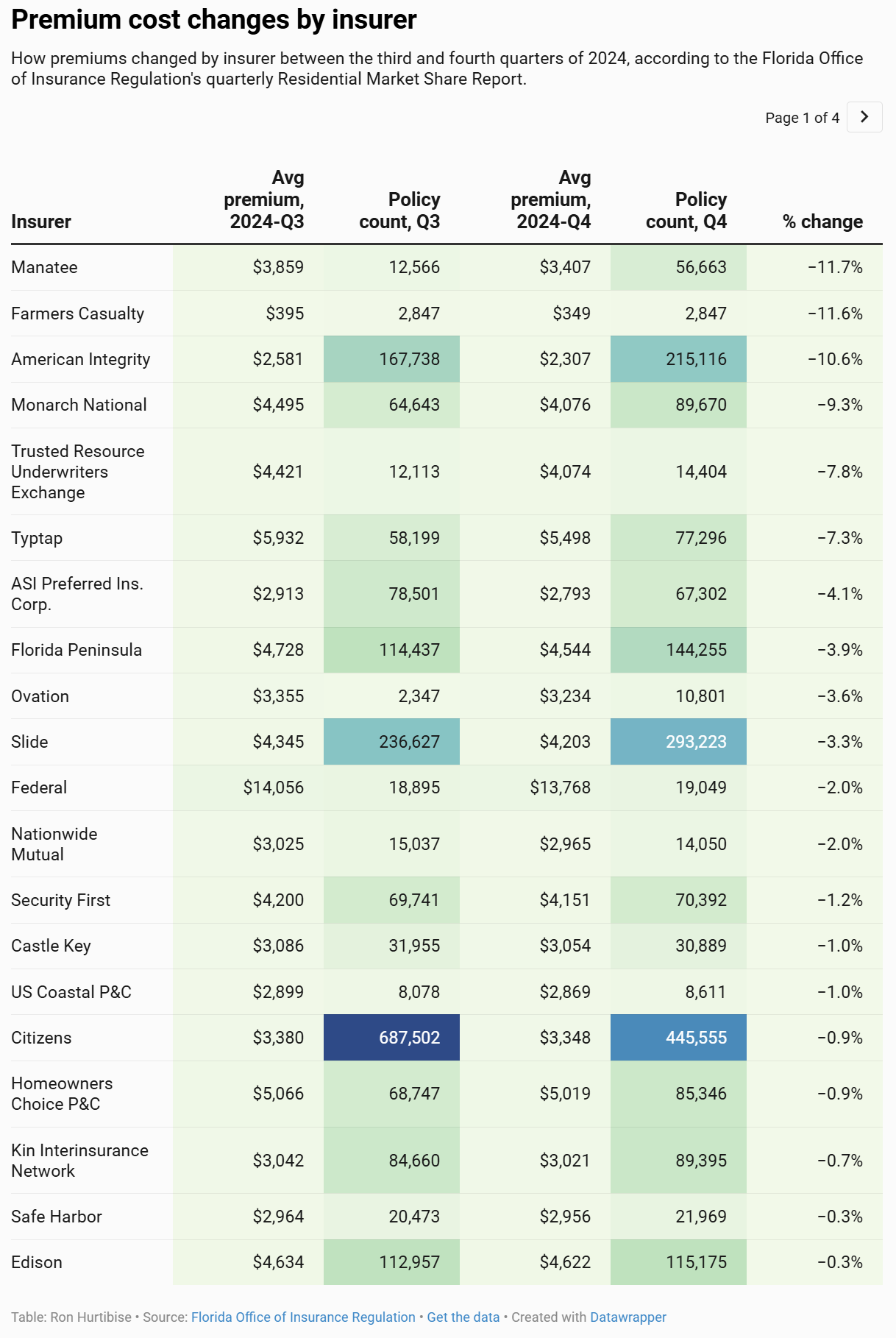

The Sun Sentinel article includes a multi-page chart (below) showing premium reductions of as much as 11.7% among some of Florida’s largest companies. Insurance Commissioner Michael Yaworsky told lawmakers recently that since the beginning of 2024, 17 companies filed for rate decreases and 34 filed for no rate change (0%), following two years of double-digit rate increases.

The Sun Sentinel article includes an interview with Stacey Giulianti, Co-Founder and Chief Legal Officer for Florida Peninsula Insurance, which saw a 3.9% decline in average homeowner premiums. Giulianti said the decline reflects the legislative reforms that reduced the costs of runaway litigation that his company is now passing along as savings back to its customers.

“As experts have been predicting for the last few years, the strong actions of the Florida Legislature and governor to decrease frivolous litigation are starting to show solid reductions in personal residential insurance rates,” Giulianti said. “This pro-consumer trend will continue, unless the Legislature makes the big mistake of reversing it in the current session.”

The net industry average premium for multiperil homeowners insurance was reduced from $3,668 to $3,644. The net average premium for condominium unit insurance declined for the first time as well by 1.7%, from $1,737 to $1,707. Average premiums for condo associations fell for the second time in a row, by 2.5%, following a 3% decline in the prior quarter.

The OIR report is a year-end statewide commercial and personal lines summary, including policy counts. It has details on numbers of open and closed claims, pending claims, and claims where appraisal, arbitration, mediation, and alternative dispute resolution were invoked.

![]() LMA Newsletter of 3-24-25

LMA Newsletter of 3-24-25