Reforms are working in lowering rates

Florida Insurance Commissioner Michael Yaworsky testifies before the Florida House Insurance & Banking Subcommittee on November 18, 2025. Courtesy, The Florida Channel

Florida Insurance Commissioner Michael Yaworsky has been on the road, engaging with stakeholders in our state marketplace. The most recent examples: traveling with the governor to meet with reinsurers in Bermuda at the PwC Insurance Summit, and updating Florida legislators on market developments. He knows that to get work done, you need to communicate – with a wide range of constituents.

Before the Thanksgiving holiday, Yaworsky went before both insurance committees of the state legislature to report the positive outcomes to date of the legislature’s 2022 and 2023 reforms. His message to the House Insurance & Banking Subcommittee and the Senate Banking and Insurance Committee was clear: the consumer and litigation reforms have worked, resulting in rate decreases in both property and automobile insurance, more available homeowners insurance, lower reinsurance rates, a return to profitability for insurance companies, and a successful depopulation of taxpayer-backed Citizens Insurance.

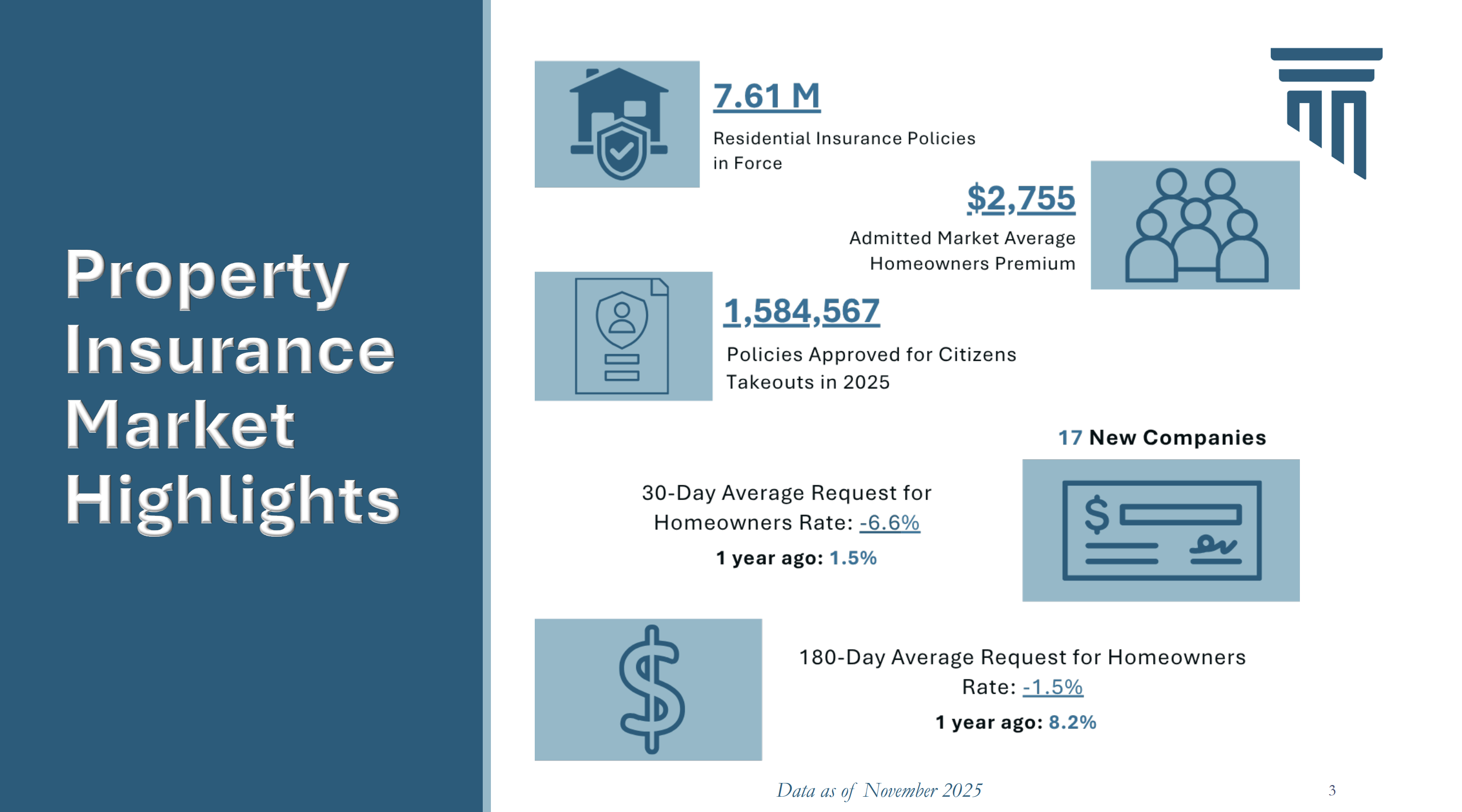

Yaworsky shared the below graphic with lawmakers, showing the 30-day average homeowners rate requested by carriers is -6.6%, compared to +1.5% a year ago, and a considerable turnaround from the double-digit increases of 2020-2022. He said he expects rate decreases to continue and he set the record straight again that the average annual homeowners premium in Florida is $2,755 − not the $4,500 to $8,000 appearing in some media publications. Yaworsky told legislators that the same litigation reforms have resulted in filed auto rate decreases of up to 17.6%.

From: Florida Office of Insurance Regulation

Yaworsky reminded lawmakers that the reforms also increased the authority and power of the Florida Office of Insurance Regulation (OIR), resulting in greater accountability by insurance companies. This includes more market examinations and investigations, with the power to take corrective action to protect insurance consumers from unlawful or harmful business practices. He said that OIR’s Market Conduct Unit has initiated over 100 examinations, completed more than 340 investigations, and secured $14.5 million in consumer restitution.

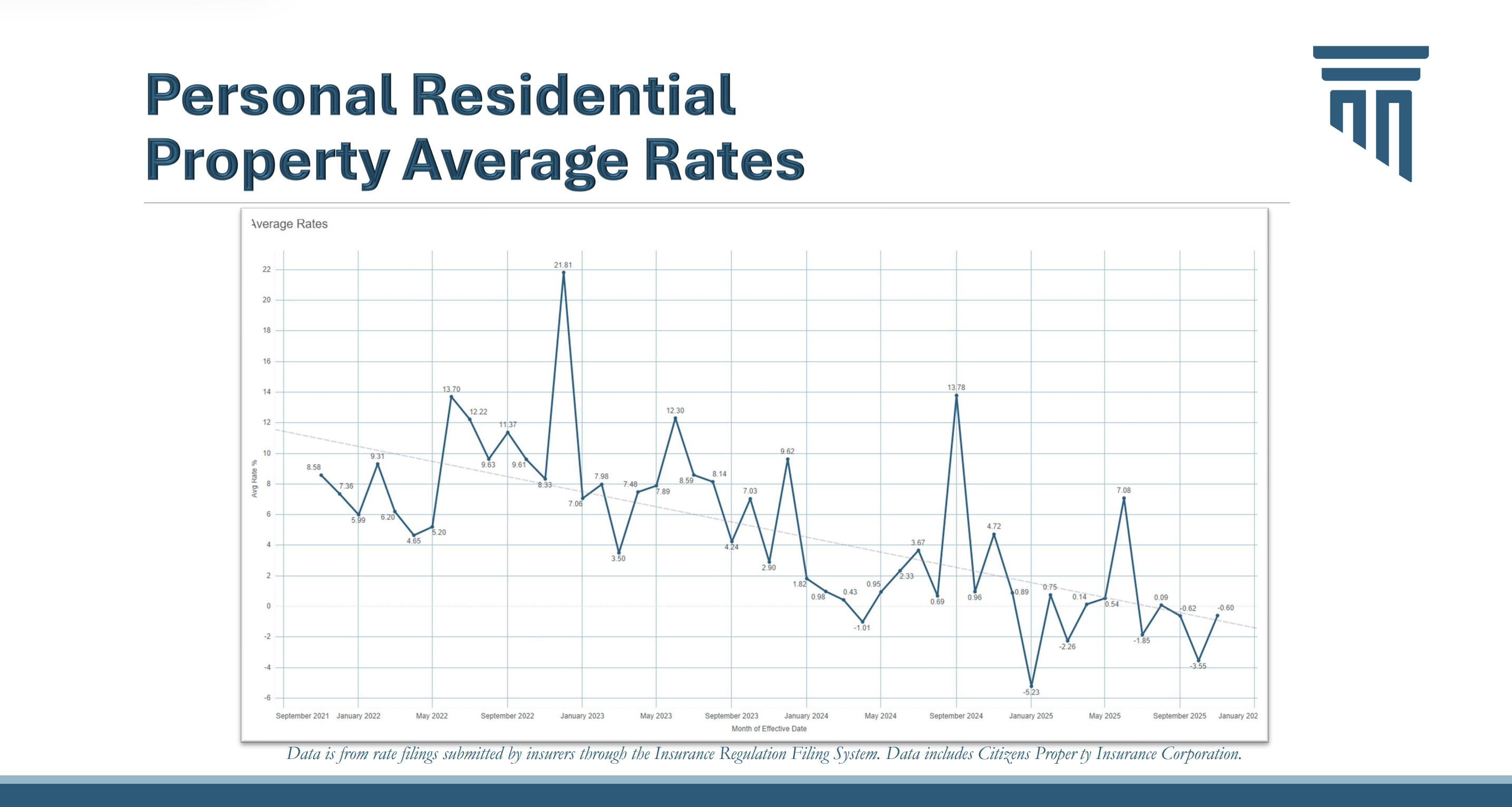

He also provided data showing that the reforms have re-righted the property insurance market as a whole. Florida’s insurance companies writing our 7.6 million residential policies are on solid financial footing, with positive net income and underwriting gains, and are once again profitable. Yaworsky stressed that’s a big turnaround from 2017-2022, when net income and underwriting gains were negative. Average personal residential property insurance rates are decreasing as a result, per the chart he shared below. The 180-day average homeowners insurance rate request is -1.5%. Yaworsky told lawmakers that while inflation is putting upward pressure on rates and has a direct impact on premiums, rates are still coming down.

From: Florida Office of Insurance Regulation

Yaworsky’s slide deck from the committee meetings include the latest Florida market information on policies in force, the admitted and non-admitted companies’ market share, industry performance in terms of net income, underwriting gains, and combined ratios, total insured value, direct written premium, and more.

Yaworsky took questions from lawmakers, some of whom are property insurance lawyers, skeptical about whether the legal reforms went too far. He was asked whether the reforms, including the elimination of one-way attorney fees for plaintiff lawyers, were preventing consumers from hiring lawyers to sue in claim disputes. Yaworsky responded that he and OIR have seen no systemic evidence of that. He also pointed out that Florida still has a disproportionate share of homeowners insurance litigation, despite the reforms, although it’s getting better. OIR’s latest Property Insurance Stability Report shows that in 2023, Florida had 9.7% of the nation’s homeowners insurance claims yet 71.5% of the homeowners insurance lawsuits.

Yaworsky also took questions on:

- The Florida Hurricane Catastrophe Fund – He was asked whether the current retention point and capacity of the Cat Fund should be lowered to make affordable reinsurance more available for carriers. Yaworsky said that some “serious thinking” needs to be done about the Cat Fund’s role but with thoughtful deliberation.

- Managing General Agents (MGAs) & Insurance Company Affiliates – He was asked whether OIR is looking into the financial arrangements between property insurance companies and their parent companies, including affiliate payments of MGA’s, an issue raised earlier this year. Yaworsky replied that OIR is not, as one was not funded in the last legislative session, and that the OIR study from 2022 was not valid. He said OIR is mindful of capital flow between insurance companies and their parent corporations and included language to define “fair and reasonable” fees in an agency bill last session. Ironically, that bill died when lawmakers inserted late language to repeal the litigation reforms.

- OIR Proposed Legislation for 2026 – Yaworsky didn’t share any particular proposals that he and OIR may be formulating for the upcoming legislative session that begins in January 2026, but stressed four goals that OIR is focusing on: Home resiliency and code plus adoption (to achieve premium savings for homeowners who make improvements); Strengthening OIR; Policyholder protection and education (including an overhaul of the myriad of disclosures included in policies); and a Stable, predictable, and reliable marketplace.

Yaworsky said OIR is looking into how Artificial Intelligence is being used by insurance companies. He also mentioned that OIR is conducting a study on the seven property insurance companies that went insolvent between 2021-2023.

The Florida Senate Banking and Insurance Committee meeting schedule

We applaud the commissioner’s thought leadership. Of the six weeks of legislative committee meetings concluding this Thursday afternoon, the Florida Senate has had but one meeting of its Banking and Insurance Committee (featuring Yaworsky’s presentation). But in the Florida House, there have been four meetings; puzzling, given the commissioner has indicated that no further reforms are needed and that existing areas of concern are being addressed by OIR.

On the consumer side, our biggest challenge is communicating the difference between “rate” and “premium.” I have been regularly interviewed by news media, most recently telling WFLA-TV in Tampa that “These premiums will eventually level off, even though the rates are down, premiums are still up because of inflation.” An $8 piece of plywood pre-COVID, today goes for $23.

In a recent Sun Sentinel article noting the downward rate trend, Stacey Giulianti, Co-Founder and Chief Legal Officer for Florida Peninsula Insurance, summed-up well the relationship between rate and premium, even as rates decrease. “I cannot predict what the cost decrease will be because (a) inflation may push the value of the home up in terms of repairs costs, and (b) individual customers add or change coverages, upgrade packages, add animal protection, etc.”

![]() LMA Newsletter 12-8-25

LMA Newsletter 12-8-25