Plus, a new report on Florida’s post-reform insurance saving

Fresh concerns about Florida insurance regulators’ revamped wind mitigation inspection form, new research on the cost savings from the property insurance market reforms plus a prediction on future savings this year, reduced catastrophe losses are driving continued industry improvements, plus the Florida Legislature considers a bill to ease the insurance employee shortage. It’s all in this week’s Property Insurance News.

Fresh concerns about Florida insurance regulators’ revamped wind mitigation inspection form, new research on the cost savings from the property insurance market reforms plus a prediction on future savings this year, reduced catastrophe losses are driving continued industry improvements, plus the Florida Legislature considers a bill to ease the insurance employee shortage. It’s all in this week’s Property Insurance News.

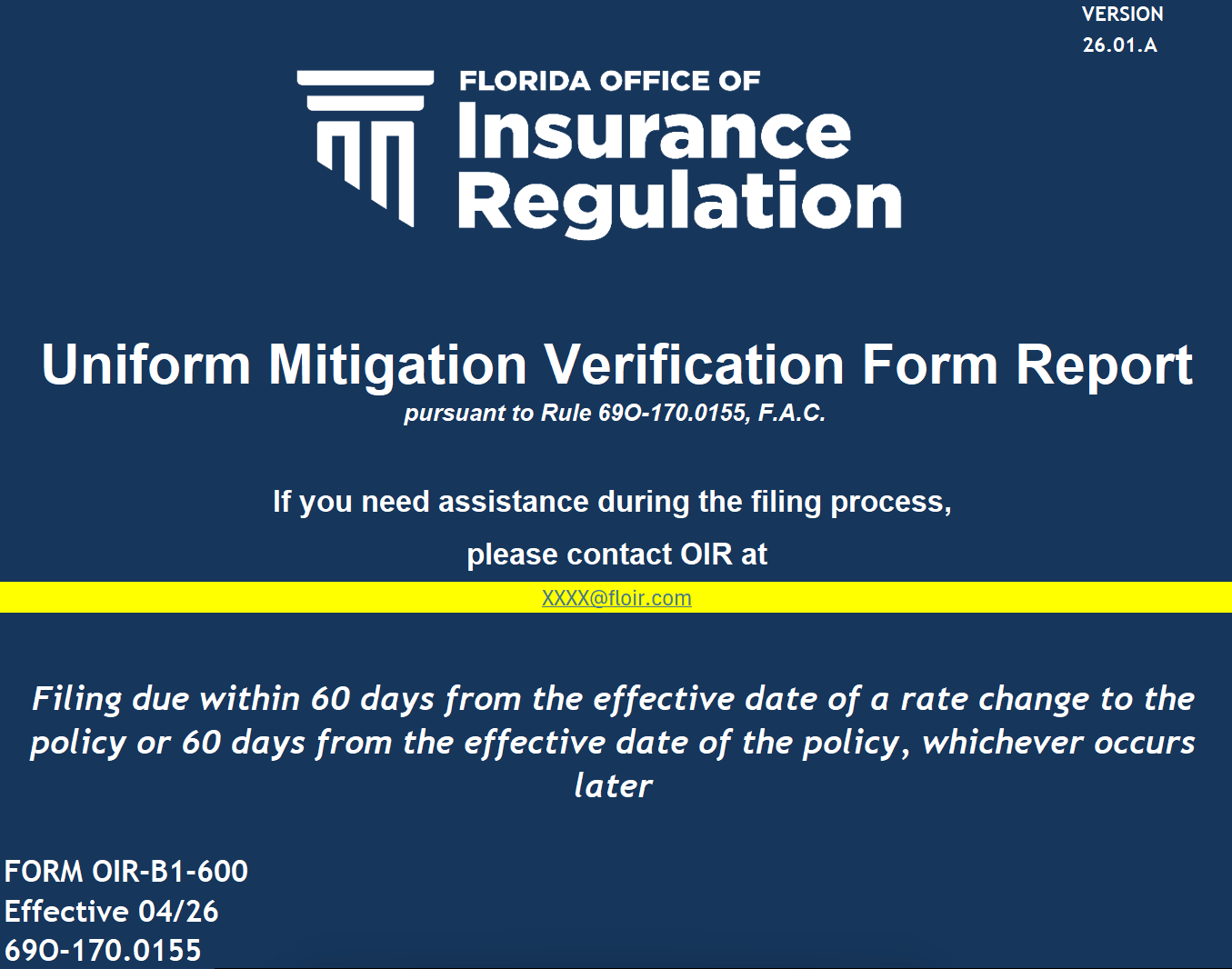

Revamped Form: The Florida Office of Insurance Regulation (OIR) will hold a rule workshop today (February 16) at 8:30am to address a loose end from this past fall’s series of rule and form changes. Rule 69O-170.0155 was changed, which included an updated Uniform Mitigation Verification Inspection Form (Form OIR-B1-1802) for insurance companies to use with their policyholders in determining hurricane mitigation discounts, as we explained in our September special report. Insurance companies must submit the form within 60 days of a rate change or 60 days from the effective date of the policy, whichever is later. The method for submitting the form was still up in the air – until now. OIR has released this reporting tool/spreadsheet titled Uniform Mitigation Verification Form Report (Form OIR-B1-600), with an effective date of April. We noticed that many of the fields under the “Data Call” tab match those in the actual Inspection Form 1802.

Revamped Form: The Florida Office of Insurance Regulation (OIR) will hold a rule workshop today (February 16) at 8:30am to address a loose end from this past fall’s series of rule and form changes. Rule 69O-170.0155 was changed, which included an updated Uniform Mitigation Verification Inspection Form (Form OIR-B1-1802) for insurance companies to use with their policyholders in determining hurricane mitigation discounts, as we explained in our September special report. Insurance companies must submit the form within 60 days of a rate change or 60 days from the effective date of the policy, whichever is later. The method for submitting the form was still up in the air – until now. OIR has released this reporting tool/spreadsheet titled Uniform Mitigation Verification Form Report (Form OIR-B1-600), with an effective date of April. We noticed that many of the fields under the “Data Call” tab match those in the actual Inspection Form 1802.

Concerns are being raised at the thought of manually inputting thousands of these forms into the OIR reporting tool/spreadsheet. There is also ambiguity whether a consumer’s current wind mitigation form would have to be redone if it’s within its current five-year allowable shelf life. Will consumers have to have a new inspection, too? OIR had acknowledged that’s something it needed to make a final call on. We at LMA are hopeful that the inspection firms themselves could upload their data into the OIR portal instead, and for the 25% of the handwritten forms, that we can work on another solution.

Another issue: OIR has not released updates on related forms required to fully carry out this program, including the actual mitigation discount credits (Forms 1699 and 1700), and the discounts schedule (Form 1655) that insurance companies will use to generate and communicate the policy discount to the consumer. We welcome our readers’ comments as we’ll be participating in the workshop and will publish a report on the outcome. You can join the workshop yourself by dialing (850) 328-4354, then inputting code 350 928 043#.

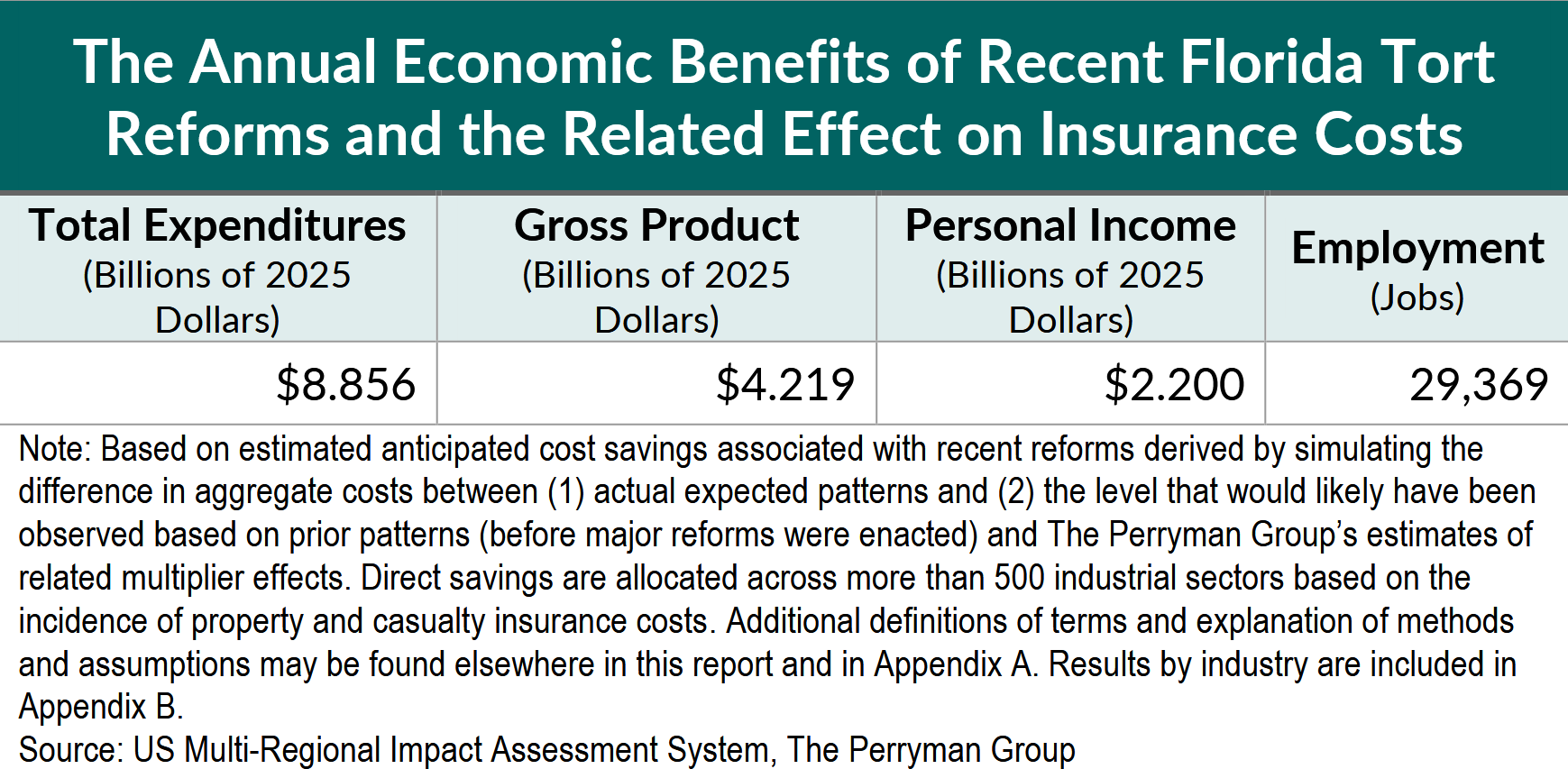

Reforms Lowered Costs: The Florida Legislature’s 2022 and 2023 property insurance consumer and litigation reforms lowered today’s costs by about 14.5% more than they would have been without the reforms. That’s according to a new research report by The Perryman Group. “Recent Florida reforms have reduced excess tort costs and the burden they have on individuals, the economy, and society,” the report concluded. It notes the reforms also attracted new insurance companies to Florida, increasing consumer choice, and freed up money for other investments. Savings from reductions in insurance costs associated with tort reform led to an estimated increase in Florida business activity of more than $4.2 billion in annual gross product.

Reforms Lowered Costs: The Florida Legislature’s 2022 and 2023 property insurance consumer and litigation reforms lowered today’s costs by about 14.5% more than they would have been without the reforms. That’s according to a new research report by The Perryman Group. “Recent Florida reforms have reduced excess tort costs and the burden they have on individuals, the economy, and society,” the report concluded. It notes the reforms also attracted new insurance companies to Florida, increasing consumer choice, and freed up money for other investments. Savings from reductions in insurance costs associated with tort reform led to an estimated increase in Florida business activity of more than $4.2 billion in annual gross product.

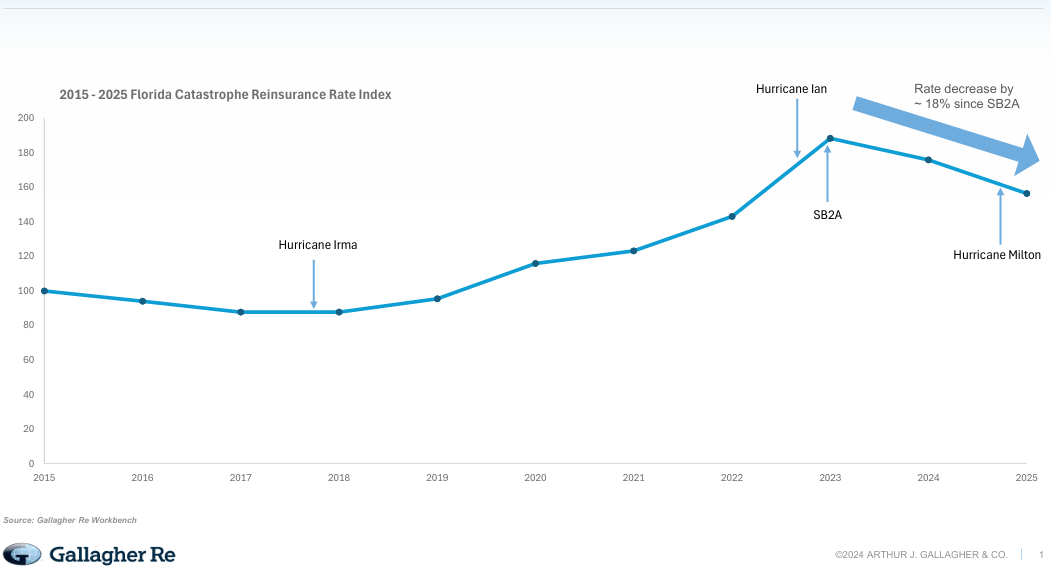

Source: Gallagher Re (click to enlarge)

Future Property Insurance Savings: Someone who knows intimately about those savings is Adam Schwebach, broker and head of property for North America at Gallagher Re, the global reinsurance broker. He told the Insurance Journal there have been “undeniable” impacts from Florida’s reforms, and that the price of reinsurance should continue its decline for the upcoming June 1 renewals for hurricane season. Up to 40% of a policy’s cost is reinsurance, so that’s a big deal. In the article, Schwebach also shared some news from Gallagher Re’s recent annual Florida broker summit, and his views on the Florida Hurricane Catastrophe Fund and Citizens Property Insurance.

![]() Property Insurance Industry Stronger: The reinsurance industry’s technology partner, data-driven Verisk, is out with its underwriting results for the U.S. property and casualty insurance industry through the third quarter of 2025. Here’s what’s up: written premiums (by 5.1% to $740.7 billion); earned premiums (by 6.9% to $711.2 billion); net underwriting gain (of $35.3 billion compared to $4 billion in the same period in 2024); and surplus (increased to $1.2 trillion from $1.12 trillion). What’s down: the rate of incurred losses and loss adjustment expenses (increasing just 0.6%, compared to a 2.7% rise in 2024). For the first time in a decade, the combined ratio has fallen below 95 through the third quarter (to 94% from 97.9% in the year prior).

Property Insurance Industry Stronger: The reinsurance industry’s technology partner, data-driven Verisk, is out with its underwriting results for the U.S. property and casualty insurance industry through the third quarter of 2025. Here’s what’s up: written premiums (by 5.1% to $740.7 billion); earned premiums (by 6.9% to $711.2 billion); net underwriting gain (of $35.3 billion compared to $4 billion in the same period in 2024); and surplus (increased to $1.2 trillion from $1.12 trillion). What’s down: the rate of incurred losses and loss adjustment expenses (increasing just 0.6%, compared to a 2.7% rise in 2024). For the first time in a decade, the combined ratio has fallen below 95 through the third quarter (to 94% from 97.9% in the year prior).

Rep. Brian Hodgers (R-Viera). Courtesy, Florida House of Representatives

More Insurance Workers Needed: Rep. Brian Hodgers is sponsor of HB 1343, which now awaits a floor vote by the Florida House of Representatives. A companion bill in the Senate has made it through two of its three committees. It establishes a half-credit high school elective in insurance and personal finance that satisfies pre-licensure education requirements for the customer service representative (4-40) license, needed to work as a salaried employee of a general lines agent or agency in Florida. Hodgers, an insurance agent who runs his own agency, hopes the bill will ease the shortage of employees. He told the Insurance Journal about the difficulty that agencies across the state have had in hiring and retaining customer service reps.

A reminder that you can easily share this or any other story with your friends & colleagues by clicking the red SHARE THIS button below or Share this entire newsletter edition.

![]() LMA Newsletter of 2-17-26

LMA Newsletter of 2-17-26

![]()