We Have Been Carrying the Water, Now It’s Time to Pick Up the Bucket!

For those of you who closely follow LMA’s work, you have heard me say over and over again that the “graying” of our insurance industry workforce (yes, as the old TV commercial used to say,

“only my hairdresser knows”!) is posing a huge challenge in many respects from claims handling to underwriting to operations. The venerable and seasoned workforce that has “been there” through thick and thin are retiring or moving into part-time positions. In essence, these insurance warriors have been carrying the insurance industry’s water for a long time.

As I traveled the state the past two weeks visiting insurance villages and adjuster training sessions (you can watch my travelogue video here), I reconnected with so many of those who I saw in the field in the 2004 and 2005 storms and for that matter during Hurricane Andrews! One Vice President of Claims sat with me for a few minutes in the 95 degree heat under a canopy and lamented that it’s so tough to get the younger generation involved in the insurance industry. He said, “Geez, this business is practically recession proof because we all have to have insurance. It’s not like we can just trim insurance coverage out of our budget. We have to have it and other things will be sacrificed when the time comes. So, for the life of me, we have been carrying the water (for the insurance process to work in our country) and now it’s time for the younger generation to pick up the bucket”!

There is no greater time than now for the generation after me to take the 40 hour insurance adjuster course and for that matter, shadow an insurance agent for a couple weeks to watch how the insurance industry works. I was contacted by Broward College just last week and they offer this online adjuster training course to help those dip their toe in the water and encourage students to pick up the bucket. If you know of young guns who want to join the ranks of incredible professionals who want to leave a legacy, please let us know and we can mentor and encourage them.

Irma’s Aftermath Becoming Clearer

Tens of thousands of more flood claims expected

Exactly two weeks after Hurricane Irma hit the mainland of Florida, all of the electricity is back on and it’s clearer that this was a higher frequency but lower impact storm claims event than initially feared. Wind to flood claims are running about 3:2 but that only considers those of course who had flood insurance, either from the National Flood Insurance Program (NFIP) or from private flood carriers. Here’s a look at where we stand today in the key areas of Damage & Claims, Regulation, Legislation, Litigation, and Recovery.

Damage & Claims

Damage & Claims

- Total Estimated Insured Losses as of late this past Thursday were $4.2 billion

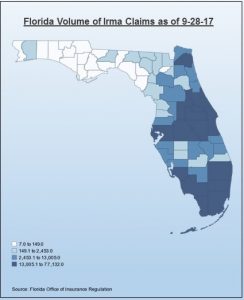

- 644,908 claims have been filed, with 16.7% closed. This Office of Insurance Regulation chart shows that Miami-Dade, Orange, Broward, Lee, Collier, Brevard, and Polk were the counties with the highest claims count.

- 1,419 of the above claims were flood claims filed with private carriers. In addition, FEMA reports 17,000 flood claims have been filed with the NFIP as of last week, with nearly 20% from Monroe County (the Florida Keys) and 10% from Duval County (Jacksonville), with Miami-Dade, Lee, Collier, and St. Johns Counties making up the bulk of the remainder. NFIP Director Roy Wright toured Jacksonville after Irma, afterward saying he expects tens of thousands of more flood claims in the coming weeks.

- For those without flood insurance, there is federal aid through grants that require no payback, but the maximum grant is $33,300, with the average paying $4,000 to $6,000 – rarely enough to fully repair/rebuild. FEMA has warned that required home inspections that normally occur 7-10 days after an application is approved are now taking up to a month.

- Citizens Property Insurance Corporation, the state’s insurer of last resort, reports fewer claims than expected. As of last Wednesday, it had received 45,681 claims, which it expects to swell to 70,000 claims over the next year or two, with a likely insured loss overall of about $1.23 billion.

Regulation

- The OIR Emergency Order of September 13 that froze rates and cancellations along with various filing requirements for 90 days, created some confusion within the insurance industry. Last week, OIR released this Q&A document in response to some of the most frequently asked questions.

- The Florida Office of Insurance Regulation (OIR) published the 5 bulletins issued by FEMA September 12 addressing the claims process for its National Flood Insurance Program (NFIP) Hurricane Irma policyholders. Click here for a summary of the bulletins and further links.

- OIR is warning homeowners not to sign Assignment of Benefits (AOB) agreements with contractors when ordering Irma repair work. Its recent press release offers consumer tips and encourages homeowners to file a claim directly with their insurance company to maintain control of their policy.

- CFO Jimmy Patronis is urging businesses to put pressure on their local state legislators to pass meaningful AOB reform this year, the fifth year such bills are being filed (more in Bill Watch) He’s also sending anti-fraud strike teams across the state to protect Floridians from post-storm fraud.

- Facebook is full of companies that want policyholders to sign AOBs. If you see examples of them like this roofing company, please forward them to me. I am working with media on a consumer education campaign, as others are doing too, so that we can get the ‘NO AOB’ message out. Results so far have included this great AOB story by the Orlando Sentinel.

- The IRS has announced Hurricane Irma – Tax Relief Provisions Provide Extensions to January 31, 2018. This includes a broad list of individual, business, estate and trust income tax, gift tax, employment and certain excise tax filing and payment obligations, including quarterly estimated tax payments.

Legislation

Florida House Speaker Richard Corcoran has created a Select Committee on Hurricane Response and Preparedness to consider critical issues related to state disaster policy. Among those issues, said the Speaker, were protection of the elderly, disabled, and other vulnerable populations as well as to look at evacuation and mitigation challenges for future storms. This follows the death of eight residents of the Broward County nursing home left without air conditioning post-Irma. Read the Speaker’s Memo here.

Recovery

- State Agriculture Commissioner Adam Putnam was quoted last week as saying that Hurricane Irma’s path “could not have been more lethal” to Florida’s farmers. The citrus crop was especially hard hit, with some groves reporting up to 80-90% destroyed, others 40%. Other fruit and vegetable crops suffered a 50-70% loss. Although agriculture is the state’s #2 industry, Florida is one of the least insured states in the country by federal crop insurance.

- Florida’s #1 industry – tourism – is faring better post-Irma. Indications are that impacts to the $100 billion industry will be short-term and won’t affect this winter’s tourism season which begins just before Christmas.

Litigation

Power came back on, but two law firms filed a lawsuit that seeks class-action status to represent Florida Power & Light customers who paid storm charge fees that were supposed to cover hurricane preparation work. The suit claims FPL charged $2 to $10 per month that was earmarked to pay for clearing trees near power lines and placing power lines underground. Instead, almost 5 million FPL customers, including nearly 500,000 in Southwest Florida, lost power when Hurricane Irma barreled into the state. We will keep you apprised of this developing story.

Private flood insurance: US Senate Kills the Idea for Now

NFIP reauthorization running out of time

On Thursday, September 28, 2017, the U.S. Senate approved a must-pass bill to reauthorize the Federal Aviation Administration (FAA) and at the same time, removed language in the bill that was aimed at fostering a private flood insurance market. The flood language, commonly referred to as the Ross-Castor bill after sponsors Dennis Ross (R-Florida) and Kathy Castor (D-Florida), passed the House last year by a vote of 419-0 and was adopted this session by the House Financial Services Committee three months ago by a vote of 58-0. As a matter of fact, earlier in the day on Thursday, the U.S. House of Representatives approved (by a vote of 264-155) the FAA reauthorization bill, which included the private flood insurance provision. But Senators Bill Cassidy (R-Louisiana) and John Kennedy (R-Louisiana) effectively killed the Flood Insurance Market Parity and Modernization Act from the FAA reauthorization bill, issuing a statement that they wanted to push for comprehensive reform versus piecemeal reform.

In fact, Democratic Ranking Member of the Committee on Financial Services Maxine Waters (D-California) stated that moving this bill, at this time, while ignoring all the other policy responses needed for the flood insurance program and the ongoing natural disasters in our country, was simply irresponsible.

In essence, those who wanted the private flood insurance language cut said Congress needed to address the larger issue of creating a long-term solution to the National Flood Insurance Program (NFIP). Those close to the situation, however, said the real reason the Louisiana senators fought the flood insurance bill’s successful passage was because rates would have increased for repetitive loss properties. As it stands now, the NFIP will expire on Dec. 8, 2017.

Why We Will Miss Bryan Koon

Director of Florida’s Division of Emergency Management departs

Bryan Koon (in sunglasses), looks on during Post-Irma visit to Jacksonville with Governor Scott.

Last week, Governor Rick Scott announced that Bryan Koon, Florida’s long-time and outstanding Emergency Management Director, was leaving the post to work with a private company. It has been a privilege to work with and beside Bryan and bridge our respective disciplines, mine in insurance and his in emergency management.

His enthusiastic willingness and interest in reaching out to the insurance industry through introductions I have made for him hasn’t stopped since he first joined Florida’s Division of Emergency Management in 2011. It was then that I called him and asked if he would share a cup of coffee with me to talk about the similarities between our two industries. From then on, we have been sharing coffee and good public policy ideas ever since.

Bryan does not know the word “no.” He was always willing to figure out a way to engage and lean in to good ideas and learn many of the tools insurance companies use that could benefit emergency managers around the state. Nothing is more evident of that fact than his leadership in supporting private flood insurance alternatives to the federal government’s flood insurance program, understanding that flood insurance models can be as or more important than the current FEMA flood mapping system. Bryan also has been a leader in making communities more resilient to the wind and ravages of rising flood waters and pushed for a comprehensive flood mitigation outreach program statewide.

Hat’s off to you Bryan. We will continue to cheer you on and appreciate all of your service to the great State of Florida!

Florida Health Insurers Request 45% Rate Increase in 2018 Obamacare Policies

OIR points out the feds will subsidize that

The Florida Office of Insurance Regulation (OIR) announced last week that the remaining nine companies offering PPACA-compliant plans for 2018 are asking for an average 44.74% rate increase over their 2017 individual major medical plans. OIR in its release was quick to point out that the majority of this increase though – 31% – is directed at the popular Silver plans, which are 70% of Florida’s market and subject not only to premium subsidies, but the only plans eligible for additional federal cost-sharing reductions, which help reduce a policyholder’s deductible and maximum out of pocket expense. OIR said the non-Silver plans will increase an average of 18%.

Quoting from OIR’s release: “Most consumers with the Silver plans will not see an out-of-pocket change, as the federal premium subsidy will also increase to absorb this extra cost. In fact, as noted in the documents linked below, a family of four earning $53,000, as well as an individual earning $27,000, may see a slight decrease in their out-of-pocket health insurance premium in 2018.”

OIR said those consumers enrolled in a Silver on-Exchange plan that do not receive a premium subsidy will have the option of purchasing a similar off-Exchange Silver plan without this extra cost. But for comparison: in 2013, an unsubsidized plan comparable to an existing Silver plan would cost a family of four an average of $7,200. In 2018, the average unsubsidized cost for the same family totals $17,000, according to OIR.

As Obamacare has become more expensive and more heavily subsidized by the federal government, the number of participating carriers in Florida has declined steadily since the new system went into effect in 2015. There were 21 companies participating in 2015, 19 in 2016, 14 in 2017, and nine for the coming 2018. Of those nine, only six are offering on-Exchange plans. As a result, Florida will have 42 of its 67 counties that are served by only one carrier in 2018.

FBI Targeting South Florida Attorneys for Insurance Fraud

PIP today, AOB tomorrow?

Five South Florida personal injury lawyers, arrested and charged with insurance fraud by the Broward Sheriff’s Office have caught the eye of the FBI in what is now a widening investigation of an insurance fraud ring involving Personal Injury Protection (PIP) claims from automobile accidents. Police say all five lawyers are on tape taking kickbacks from medical facilities who were part of the scheme.

Five South Florida personal injury lawyers, arrested and charged with insurance fraud by the Broward Sheriff’s Office have caught the eye of the FBI in what is now a widening investigation of an insurance fraud ring involving Personal Injury Protection (PIP) claims from automobile accidents. Police say all five lawyers are on tape taking kickbacks from medical facilities who were part of the scheme.

The five are accused of paying tow truck drivers and auto repair shops to solicit accident victims and then in cahoots with two medical practices – Margate Physicians and Broward Spine Associates in Plantation – making fraudulent PIP claims on behalf of the victims. The attorneys are collectively charged with various counts of patient brokering, organized crime to defraud, solicitation, conspiracy, and the use of a two-way communication device. Five tow truck drivers and auto repairers were also arrested.

Arrested were Steven Slootsky of Steven E. Slootsky P.A of Boca Raton; Alexander Kapetan Jr., of Wites & Kapetan of Lighthouse Point; Vincent Pravato of Wolf and Pravato of Davie; Mark Spatz of Simons & Spatz, Davie; and Adam Hurtig of the Hurtig Law Group of Ft. Lauderdale. Hurtig, said police, took things a step further and reportedly had a fee-splitting agreement with the medical practices where he would covertly take a portion of his clients’ settlement funds as kickbacks, after their medical bills were paid. Officials say the group received more than $521,000. More arrests are expected.

The Need for Speed

Federal study points to need for states to take speeding more seriously

We often hear about The National Transportation Safety Board (NTSB) and pay attention when we read about traffic crashes and driver habits especially if we have teenage drivers. LMA wanted to know more about the NTSB and discovered that the federal agency is celebrating its 50th year in the business of investigating transportation accidents. It determine the probable causes of the accidents, issues safety recommendations, studies transportation safety issues, and evaluates the safety effectiveness of government agencies involved in transportation.

The NTSB publishes accident reports, safety studies, special investigation reports, safety recommendations, and statistical reviews and looks at the causes of and trends in speeding-related passenger vehicle crashes and countermeasures to prevent these crashes. In a recent study, the NTSB presented several, of many, potential solutions to the issue of speeding-related crashes.

The study, Reducing Speeding-Related Crashes Involving Passenger Vehicles focused on the following five safety issues pertaining to the effective application of proven and emerging countermeasures for speeding: (1) speed limits, (2) data-driven approaches for speed enforcement, (3) automated speed enforcement, (4) intelligent speed adaptation, and (5) national leadership. From 2005 through 2014, crashes in which a law enforcement officer indicated a vehicle’s speed was a factor resulted in 112,580 fatalities, representing 31% of all traffic fatalities. Yet, the current level of emphasis on speeding as a national traffic safety issue is lower than these statistics suggest.

The study is very high on the use of “Automated Speed Enforcement”, which are radar-linked cameras that automatically take pictures of speed violators. Among the study’s recommendations: that the 35 states that prohibit or don’t utilize the practice do so, and the 15 states with it, amend current laws to remove operational and location restrictions on its use. Florida is one of the states without a law on its use.

Florida Realtors: Florida Housing Market Continues to Roar

Foreclosures down nearly half from last year

Credit: Ridofranz

Florida’s housing market is continuing to roar, says the Florida Realtors association, with all market indicators rising: an increase in closed and pending sales, more new listings, higher prices, and the sales of single-family homes statewide up 0.9% (over 25,000 more) compared to August 2016. Demand from buyers continues to grow, especially for homes in the $250,000-and-under range, but the shrinking inventory is creating affordability challenges for many first-time buyers.

The statewide median sales price for single-family existing homes in August was $240,000, up 6.7% from the previous year, and for townhouse-condo properties in August was $170,000, up 6.3% over the year-ago figure. August marked the 69th consecutive month that statewide median prices for both sectors rose year-over-year.

By comparison, in California, the statewide median sales price for single-family existing homes in July was $549,460; in Massachusetts, it was $400,000; in Maryland, it was $296,665; and in New York, it was $270,000.

Statewide closed sales totaled 9,716 last month, up 2.6% compared to August 2016 for Florida’s townhouse-condos. Closed sales data reflected fewer short sales and foreclosures last month: Short sales for townhouse-condo properties declined 39.4% and foreclosures fell 49.1% year-to-year; short sales for single-family homes dropped 34.8% and foreclosures fell 45.4%. Closed sales may occur from 30- to 90-plus days after sales contracts are written.

Inventory continued to tighten in August with a 3.8-months’ supply for single-family homes and a 5.4-months’ supply for townhouse-condo properties, according to Florida Realtors. According to Freddie Mac, the interest rate for a 30-year fixed-rate mortgage averaged 3.88% in August 2017; it averaged 3.44% during the same month a year earlier.

The Cadillac of Grocery Stores

I grew up about 12 miles from Publix grocery headquarters in Lakeland. (For our out of state readers, simply google “Publix” and you will have a ball reading about this grocery chain that is a Florida icon.) All my adolescent pals and I worked for Publix back in the day and no matter what new store opens, I still am loyal to what my grandfather called, “The Cadillac of grocery stores.” This chain has such loyalty that my colleagues and friends talk about “my Publix” or “my store” as though they own a piece of the store they shop in regularly. Publix believes that loyalty goes both ways and not only are their customers the most faithful of any I’ve seen, but Publix rewards customers for their loyalty.

A clear example of the commitment Publix has to its customers is their performance before, during and after Hurricane Irma. Many of their stores did their best to stay open despite shelves emptied by panicked customers. And when it was gonna be “awhile” before things returned to normal, Publix did its best to not miss a beat. The Publix semi-truck cavalry was seen all along interstates, along with utility trucks, making sure essential needs were available. I share this story with you because the property insurance industry was very much “Publix-like.” Insurance companies have a loyalty and duty to their policyholders and many executives had damage themselves to their homes from Irma. We will do all we can to help continue the recovery from this storm. If you have stories of individual heroes and companies, please email us at [email protected]

Hurricane Irma also delayed the start of interim committee meetings of the Florida Legislature. Next Monday, October 9, will now be the first week of those committee meetings with a super-packed agenda to make up for lost time. We’ll be watching and reporting back on developments in the next LMA newsletter. Here are links to the chambers’ calendars for next week:

House Calendar for the week of October 9

Senate Calendar for the week of October 9

See you on the road!

Lisa